TISCO Reports a 25% Profit-Dropping from Higher ECL as NPL Jumps to 3.28%

TISCO Reports a 25% Profit-Dropping from Higher ECL as NPL Jumps to 3.28%.

Tisco Financial Group Public Company Limited (TISCO) has reported its consolidated financial statement of 2Q20 through the Stock Exchange of Thailand as follows;

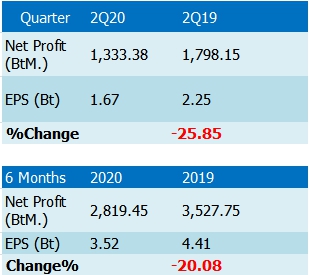

TISCO reported a net profit in 2Q20 at 1,333 million baht, decreased 25.8% YoY due to a consequence of COVID-19 outbreak to the domestic economic downturn, banking businesses have been affected from a slowdown in economic activities.

Net interest income rose due to a decrease in interest expense aligning with an effective cost management during declining interest rate environment. However, non-interest income from core businesses declined due to a slowdown in economic activities, particularly banking fee income from bancassurance business and loan-related fee income following lower new business volume.

Meanwhile, expected credit loss increased from the revision of ECL impairment model in accordance with TFRS 9 and an increase in NPLs amid the economic slowdown.

Expected credit loss (ECL) totaled 872.99 million baht, increased compared with bad debt, doubtful accounts and impairment losses of 137.54 million baht in the second quarter of 2019, and accounted for 1.50% of average loans. An increase in ECL was partly resulted from the revision of the impairment model in accordance with TFRS 9, together with an increase in non-performing loans. Nevertheless, ECL was on the decline compared to the previous quarter, in which the Company has partially set up ECL impairment against an assumption on economic outlook in advance, according to TFRS 9.

In the second quarter of 2020, TISCO reported NPLs amounting 7,480.28 million baht, increased by 1,399.68 million baht (23.0% QoQ), and accounted for NPL ratio of 3.28%, increased from 2.56% at the end of the first quarter of 2020 mainly from hire purchase loans and loans against auto licenses. The increase in NPLs was caused by the economic slowdown due to the spread of COVID-19 which impacted clients’ debt serviceability.