Keep a Close Eye on the Banking Sector for a Recovery in 1Q21 Earnings

Keep a Close Eye on BBL and KBANK for an Outstanding Gain in 1Q21 Earnings.

The banking sector is expected to publish financial statements later this month, led by TISCO on April 19, and the others in the following days.

Thai commercial banks are among the hardest-hit stocks from the coronavirus impact after a series of interest rate cuts, diminishing economic activities and temporary debt suspension.

Investors witnessed the worst financial statements in 2Q and 3Q of 2020 since the Financial Crisis more than a decade ago. However, earnings saw an uptick in the fourth quarter last year in anticipation of a vaccine rollout and a series of stimulus measures to buoy the economy.

The consensus expected the momentum of the Thai banking sector to continue in 1Q21 as the economy started to recover from the Covid-19 pandemic. Some banks such as BBL and SCB will grow from their low base in 4Q20, while KBANK will maintain a high level of profit despite its high base in the previous quarter.

Late last month, theThai cabinet approved a measure to help businesses affected by the coronavirus outbreak with soft loans and asset warehousing worth 350 billion baht in total.

The loan would help entrepreneurs to maintain their business and employment as the full reopening to boost economic recovery could be delayed to 2022. Meanwhile, the asset warehousing program would allow operators such as in hotel business to liquidate distressed assets.

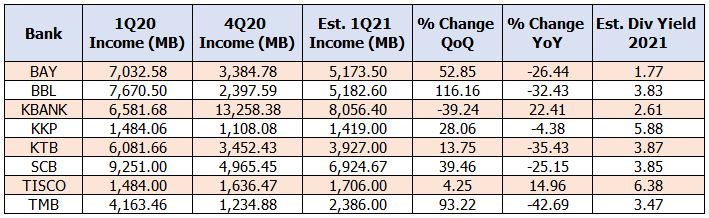

According to the consensus, BBL would lead the group in percentage gain in QoQ at +116% due to its unexpected low base in the previous quarter, followed by TMB (+93%) and BAY (+52%).

In the meantime, KBANK and TISCO would be the only two banks to report an increase in YoY at 22% and 15%, respectively.

Asia Wealth Securities (AWS) stated that the aiding measures for entrepreneurs would be active in May 2021, while having a positive view on BBL (Buy, TP Bt142.50) and KBANK (Trading, TP Bt146.50) to be the most beneficial from this measure due to higher proportion of business customers than competitors.

Meanwhile, Asia Plus Securities (ASPS) expected TISCO to report an outstanding earnings in 1Q while the others would slowly recover. The recovery in earnings would be mainly due to the decrease of the group’s credit cost from 1.66% to 1.61% as the provision in 2H20 would compensate the NIM that ASPS expected to come out close to the previous quarter due to an unchanged policy rate.

Nevertheless, ASPS still recommended TISCO with a “BUY” recommendation at a target price of Bt102.00 per share, stating that the bank has a high dividend yield. The second preferred securities would be BBL at a target price of Bt154.00 per share due to a laggarded price and a P/BV at 0.5x. As for KBANK, ASPS gave a target price at Bt155.00 per share.