DTAC Reports a Drop of 18% in 3Q Profit as D&A Rises and Revenue Falls

DTAC Reports a Drop of 18% in 3Q Profit as D&A Rises and Revenue Falls.

Total Access Communication Public Company Limited (DTAC) has reported its 3Q20 consolidated financial statement through the Stock Exchange of Thailand as follows;

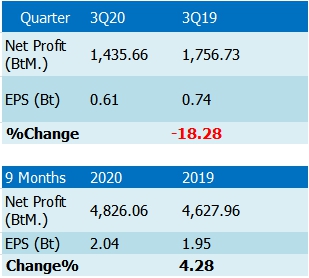

Net profit for Q320 amounted to THB 1,436 million, decreasing 24.0% QoQ from higher gain in fair value hedges and measurement in Q220, and fell 18.3% YoY primarily from higher depreciation and amortization and loss in fair value hedge.

Total revenues in Q320 amounted to THB 19,053 million, decreased slightly at 0.6% QoQ and 6.1% YoY from decline in service revenue and handsets and starter kits sales. The decrease was slightly offset by higher other operating income from TOT 2300 MHz network rental. Service revenues excluding IC decreased 1.7% QoQ and 7.6% YoY down to THB 14,375 million.

At the end of Q320, the total active subscriber base stood at 18.7 million, a decline of 107k from the end of Q220 as a result of a gradual recovery in the acquisition and better churn management. The subscriber base decline consisted of prepaid at 73k and postpaid at 34k. Approximately 32.3% of the total subscriber base were postpaid subscribers.

Service revenues excluding IC in Q320 dropped 1.7% QoQ and 7.6% YoY. Core service revenues (defined by bundle of voice and data service revenues) in Q320 declined 1.4% QoQ and 5.3% YoY as a result of prolonged economic impact from COVID-19. Blended ARPU went up slightly 0.8% QoQ and declined at 2.1% YoY in Q320.

In Q320, EBITDA (before other items) declined 4.3% QoQ and 3.0% YoY from slow recovery in revenue, increase in SG&A items from pickup in sales and marketing activities and general administrative items from their previous low level. EBITDA margin for Q320 was 40.7%. However, excluding revenues from CAT lease agreements and TOT network rental, EBITDA margin stood at 47.7%.

SG&A expenses in Q320 amounted to 3,443 million, increasing 9.8% QoQ but decreasing 6.0% YoY. The increase QoQ reflected pickup in selling and marketing activities and general administrative expense, and slightly offset.

Depreciation and Amortization (D&A) of costs of services in Q320 amounted to THB 4,849 million, decreasing 1.0% QoQ and increasing 4.1% YoY, driven by continuing network expansion.

DTAC revised guidance for 2020 on service revenue excluding IC from low-single digit decline to mid-single digit decline, while maintaining the rest which are EBITDA at 2019 level and capital expenditure of THB 8-10 billion.