A Lack of Aggressiveness in Clean Energy Business Causes BANPU a Slower Progress

A Lack of Aggressive Strategy in Clean Energy Business May Cause BANPU a Slow Progress as Coal Business Is Dying Out.

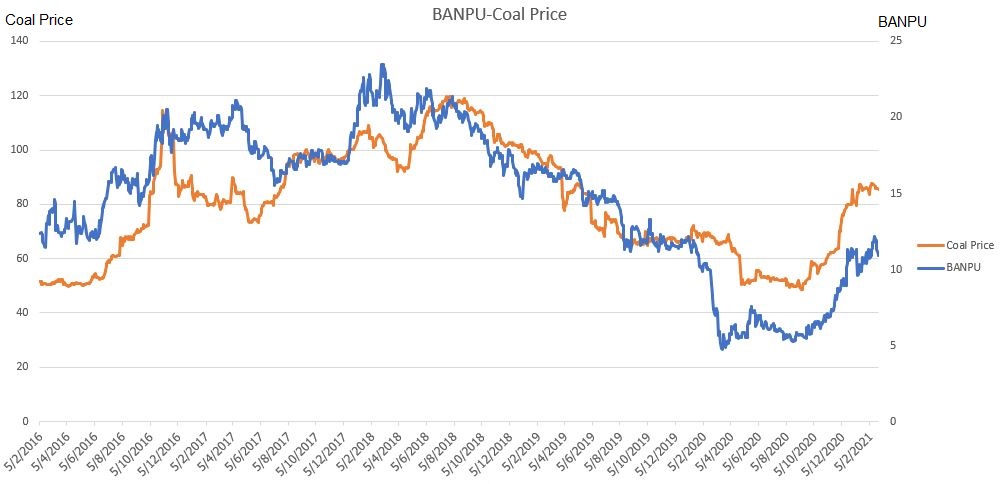

The share price of Banpu Public Company Limited (BANPU) was able to break the resistance level of Bt10.00 late last year in response to a recovery in coal prices that plunged to a record low in more than four years.

The reason for the higher coal price might be due to a decrease in supply that vanished during the coronavirus outbreak last year, coupled with the downtrend in the coal business that slowly died down.

Upon looking at the historical trading price of BANPU and coal price, which usually move in the same direction, both did not actually have a breakout year. When analysts stated that the share price of BANPU has risen in line with the sharp incline of coal price, the actual meaning of the message is “both prices have recovered to the pre-pandemic level.”

The pre-pandemic level does not sound so bad, considering some commodities and securities are struggling to recover from the coronavirus impact, but the truth is the pre-pandemic level was not a favorable situation for BANPU and the coal business, to begin with.

The coal business is dying out slowly, but quite surely as operators turn to clean energy for more greeny and goody for the mother earth. Without any new competitors, what BANPU can do is to hold on to its existing customer base as tight as possible, while increasing the revenue of clean energy in the portfolio as fast as possible.

BANPU recorded a net loss of $56 million in 2020, plunging further from a net loss of $14 million in 2019 due to lower sales and service income at $2,283 million and a one-time recognition of investment restructuring expense of $31 million from the corporatization of BKV Corporation on 1 May 2020.

Sales in the coal business decreased from $2,381 million in 2019 to $1,878 million in 2020, representing a decrease of 21% YoY. Sales from coal business was 82% of BANPU’s total revenue.

While the natural gas business recorded a 15% growth from $105 million in 2019 to $121 million in 2020, the revenue was still below the $144 million made in 2018. Sales from the natural gas business was 5% of BANPU’s total revenue.

The power and steam business recorded a revenue of $197 million, increased 10% YoY and contributed 9% to the total revenue.

Others of $88 million, decreased 8% and represented 4% of total revenue. This was mainly from the fuel trading business of a subsidiary in Indonesia.

In the meantime, coal prices are forecast to drop from $82.46 per ton in 1Q to an average of $77.1 for the rest of the year. The price is expected to rise to $78.85 per ton in 2022 and then drop to $77.45 in 2023, meaning that there will no “the share price of BANPU has risen, paralleling with a sharp incline of coal price” kind of talk anymore.

By the look of it, the situation is not favorable for BANPU.

On the bright side, BANPU will continue to record the same level or slightly lower sales revenue from coal in the next two years. During that period of time, the company will have the time for more deals or M&A to increase its production capacity in the natural business or any other businesses.

Natural gas sales volume was 113.25 billion cubic feet in 2020, increased by 64% versus 2019. This was because during 4Q20, the group consolidated sales from Barnett shale with a total of 50.93 Mcf.

Maybe this will be the core driver as BANPU advances further in the clean energy business.

But when will that be?